Accessibility Links

A perspective on recent market events

Nedbank Private Wealth reviews the latest market events where negative news and extreme share price volatility have taken centre stage.

December 2017

Over the past week, negative news and extreme share price volatility have taken centre stage. Two shares, Steinhoff, and to a lesser degree EOH, have featured heavily. While we maintain a long-term considered approach to investing, especially when it comes to equity portfolios, we appreciate and acknowledge that this negative news is unsettling for individual and institutional investors alike. This note therefore sets out our Nedbank Private Wealth equity house view positioning.

While some variables are beyond our control, we can control capital allocation and diversify

We have a valuation-based research process that includes an assessment of the company’s management. This means we pay attention to the price we pay for the future growth opportunities and risks that we assume when investing. We also always diversify because things do go wrong. They can go wrong in markets overall, and in specific companies. We can also get things wrong. To determine where to invest, the integrity of the accounting information and the reputation and track records of the management of the companies in which we invest are critical inputs. Unfortunately, as the latest media and events regarding Steinhoff appear to show: despite stringent due diligence and analysis, investment limits and risk measures, if there is a misrepresentation of facts and possibly even criminality and fraud, things will go wrong.

As an investor, you can however control your capital allocation. The diversification that we apply when we construct portfolios aims to limit the potential negative impact of share-specific news on your overall growth in the long term.

Our equity house view ensures diversification across industries, geography and currencies

We are invested in over 25 companies whose earnings come from a range of different industries, geographies and currencies. This diversification improves long-term returns, and when combined with our risk control processes, ensures that our weighting to any specific company is measured. This reduces the potential risk of overall portfolio loss due to company-specific risks.

|

Share prices versus long-term value

While it is helpful to understand specific sources of return, we believe that one must always review this in context of the overall portfolio, and relative to our weighting to a specific share. It is also important to note that in the context of our valuation-based approach, share prices can and do fluctuate relative to their true business (long-term intrinsic) value as popular sentiment (based on current headlines, social media commentary and rumours) and the markets react to the latest news (both positively and negatively). We will not invest on sentiment, but remain focussed on long-term views.

Diversification is crucial to mitigate the effect of underperforming shares

As we show in the tables below, we have had some shares in our portfolio that have under-performed but we have also owned more shares that have performed well. What these highlight, is the importance of our portfolio construction process, which ensures diversification. Diversification mitigates the negative effects of any underperforming shares on the performance of an overall portfolio.

Top contributors to performance over the past year to 8 December 2017

Naspers |

Naspers has gained 79% over the last year, and is a significant contributor to our performance over the last year. This strong performance was mainly driven by Tencent. This year’s strong run was after a negative performance in 2016 and illustrates the volatility of returns in the short term. Naspers is the largest holding in our portfolios despite continued top-slicing through the year (i.e. we have been selling down our position into share price strength). We are 12% underweight Naspers across our equity strategies relative to our benchmark weight of 30% for risk management reasons. |

Imperial |

Imperial Holdings was another strong contributor to our performance and has returned 24% over the last year. We had to endure significant volatility following the Nene-debacle, but our resilience and long-term focus have paid off for our clients and the share has gained 130% from its lows in early 2016. |

Bidcorp |

Bidcorp returned 22% over the last year following another pleasing set of results in its offshore operations. Bidcorp has been a top holding in our funds for many years (previously part of Bidvest, before the unbundling). |

| Detractors from performance over the past year to 8 December 2017 | |

Brait |

Brait has been a poor investment, and has declined 55% over the last year. Although we invested in Brait after Brexit, we underestimated the impact of Brexit, and overestimated the resilience of New Look (the subsidiary that caused the underperformance). At current levels New Look is valued at zero, and the rest of the group trades at a ~40% discount to its NAV. After the significant decline, we believe there is potential for attractive returns from current levels. |

EOH |

EOH has seen a share price performance of negative 70% over the last year (although we did not buy at these high levels). Despite reporting good results in 2017 (HEPS increased by 16%) recent corporate governance concerns relating to transactions that contribute single digit earnings to the group seem to have outweighed the good operational performance of the overall group. The full materiality of these concerns is unclear at this stage, but for now it clouds the otherwise positive outlook for Africa’s leading technology firm. |

Steinhoff |

Steinhoff International has declined by 88% since the announcement by the company that its CEO would be stepping down after accounting irregularities surfaced. This is despite a strong board and previously unqualified audits. Steinhoff has various quality assets around the world and is well positioned for the current economic upswing in Europe. Notwithstanding the share price collapse, determining a fair value in the short term that adequately prices in the breakdown of trust in management, is extremely difficult. |

Last week’s events have affected the short-term performance of our equity portfolios

While the events of the last week have contributed to what is a particularly difficult year for some of the shares in our portfolios, our overall portfolios are holding up, although the returns are below those of the market. The table that follows, illustrates the performance of Nedbank Private Wealth’s main equity strategies, both before the events of the last week, and after the market movements of the last week. In the table, our model portfolios are different reference portfolios that we use to construct portfolios for clients, but an individual client’s actual holdings may differ slightly due to their specific circumstances or tax situation.

|

One-year performance before last week (to 30 November 2017) |

One-year performance after last week (to 7 December 2017) |

Private Client Model Portfolio * |

14.4% |

7.8% |

Non-tax sensitive Model Portfolio * |

11.1% |

4.1% |

Nedbank Private Wealth Equity Fund ** |

9.1% |

3.6% |

| *Before fees and trading costs **After fees and trading costs, performance figures per Morningstar |

||

We remain long-term investors

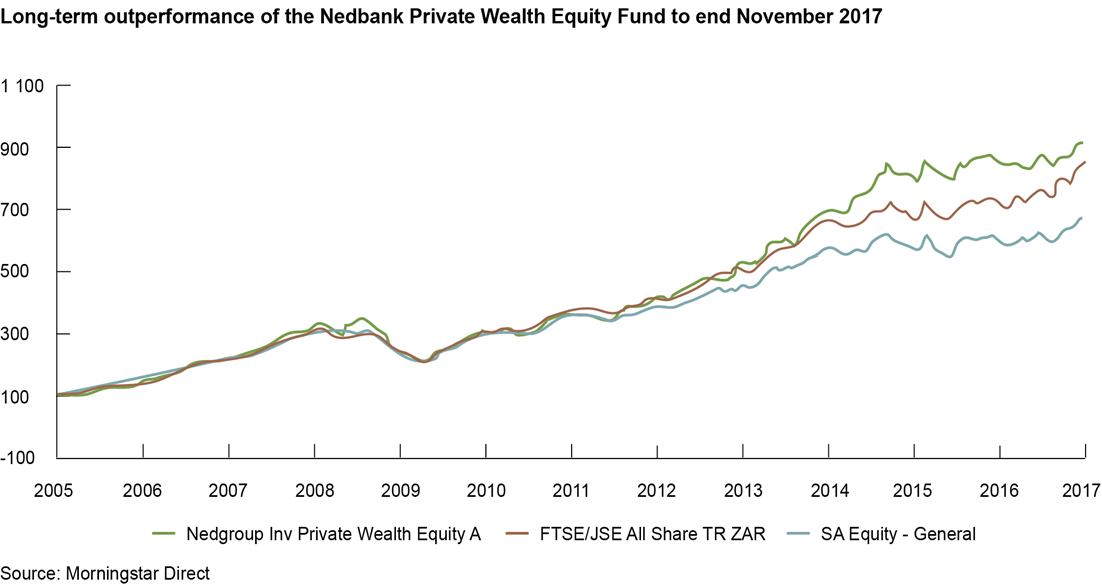

In this context, it is important to consider long-term investment performance. Over the long term, we have outperformed the market and materially outperformed our aggregate peers in the South African Equity – General unit trust category despite a tough 2017. While we will take the learnings from 2017 onboard, it is important that we remain focussed on our disciplined and proven investment process and maintain a long-term view.

|

Being an equity investor means that you are invested for the long term

There are too many uncontrollable variables in the short term that will affect returns. Long term at Nedbank Private Wealth means a rolling seven-year period. This provides enough time for investments in shares to reflect the fundamental business value of a company. Differentiating between events that will permanently destroy capital versus market events that may negatively affect the share price in the short term is crucial. As the chart above shows, it is only with time that this becomes clearer.

At Nedbank Private Wealth we have focussed our efforts on building a wealth advisory and investment process that has delivered long-term performance and will continue to do so.