Accessibilty Links

Executive Summary

The rand retraced gains and has struggled to strengthen below the R14.00 mark. Other risk assets have also given back gains, despite market expectations that President Trump’s unfavourable economic policies will likely be in gridlock after the Democrats claimed the House of Representatives in the US midterm elections. In our view, recent gains in risk assets are being overshadowed by (1) the US Federal Reserve reaffirming tighter monetary conditions (rate hikes and balance sheet normalisation in 2019), which is likely to stay as the outlook for the US economy remains positive, and (2) offshore financial conditions beginning to tighten, as reflected in the widening LIBOR-OIS and cross-currency basis spreads.

Locally, the SARB published its bi-annual Financial Stability Review report, in which the report aims to identify risks to financial stability with a view of also mitigating any vulnerabilities through macro-prudential policies and monetary policy. Four risks were identified in the report: (1) weaker global growth and risks of escalating trade wars, (2) tighter financial conditions and $-liquidity shortages, (3) weak domestic growth, and (4) cybersecurity risks. Of particular interest to us, “US dollar-liquidity shortages” were identified as having a ‘medium’ likelihood with a ‘high’ impact on the SARB’s “risk assessment matrix” for the next 12 months. We believe that these risks, and most notably $-liquidity shortages, will feed into the SARB’s response function to some degree going forward. If the $-liquidity shortage becomes a ‘high’ likelihood, interest rate hikes may be more likely to restrict/contain foreign capital, severe bouts of currency volatility and upward pressure on inflation.

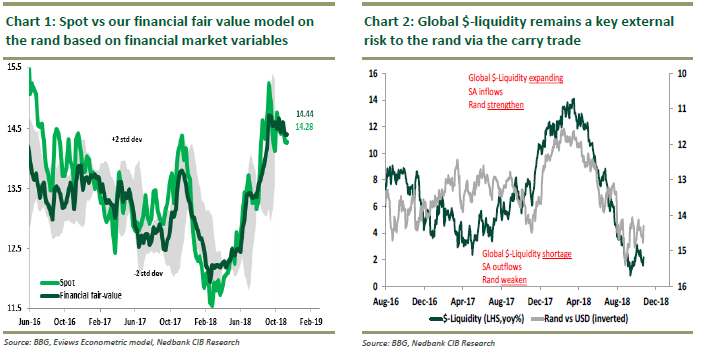

View: We believe global $-liquidity shortages (both structural and seasonal) remain a key risk to the outlook for the rand because of the US Fed’s tighter monetary policy and as demand for US dollars intensifies in the offshore US dollar banking system. As the year-end approaches, there are seasonal funding requirements (de-risking) for large European and Japanese banks stipulated by accounting regulations, which are likely to lead to a greater demand for US dollars than typically. As a result: greater demand for US dollars and rising offshore funding US dollar costs, accompanied by FX volatility, will likely not bode too well for the carry trade. The rand is one of the most liquid EM currencies, with daily forex turnover as a percentage of GDP at a staggering 18%, while SA’s trade is only less than 1% of global trade volumes. Therefore, we expect the rand to be volatile with a weakening bias towards the R14.50 area in the short term.

The structural $-liquidity shortage and the impact on financial markets remains core to our view. For more details on our assessment of global $-liquidity and its impact on SA, please refer to the following publications: Global $-Liquidity monthly dashboard assessment and Rand: All about the L world- Liquidity, 19 June 2018.

From a technical perspective, we recommend keeping an eye on the USDZAR resistance level of R14.40 and the USDZAR support level of R14.00 (please see our latest technical strategy report It is crucial for the risk-on phase that the EURUSD remain above 1.13 of 9 November 2018).