Accessibilty Links

Executive Summary

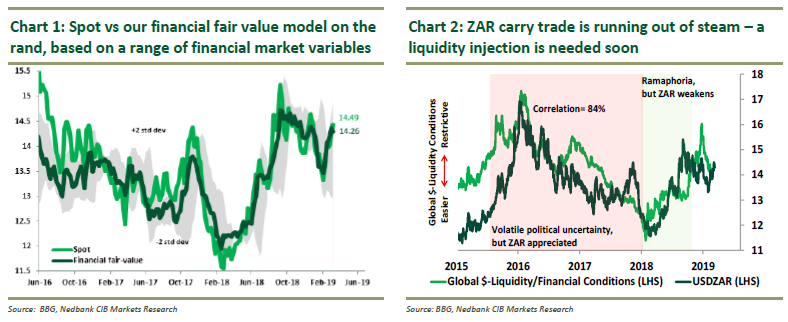

Our rand view remains unchanged – however, as Keynes said “When the facts change, I change my mind”, as such there a number of upside and downside risks on the horizon that may (or not) require us to revaluate our forecasts and trading range. Our view that the rand is likely to trade within the 14.00-14.50 range has been successful so far as we have been selling into the rand strength close to R14.00, and would buy into weakness as it approaches R14.50.

From a currency perspective: for now our base case remains- the rand is likely to trade within the R14.00-R14.50 range in the near-term as investors are likely to asses: (1) incoming data prints both locally and globally will provide investors/policy markets of the severity of the current slowdown in local/global growth which will guide or further enforce global central bank’s policy decisions (dovish tone) (2) We expect Moody’s to keep its credit rating unchanged however we do believe that there is a possibility they change the outlook from “neutral” to “negative” and notably (3) all eyes will be on the Federal Reserve policy meeting (20 March) – we believe this is an important meeting for the outlook for risk-assets. We expect the Fed to keep interest rates unchanged however market participants have already discounted this into the price of riskier assets since the start of this year after the Fed surprised markets with its dovish pivot and amid low inflation/softer economic growth. Notably, in recent months there has been a growing consensus within the Fed (FOMC speeches and published research) that “quantitative tightening” or the reduction of its balance sheet tightened financial conditions considerably last year. As such should the Fed announce a plan to end “quantitative tightening” ahead of schedule this will certainly be positive for risk-assets as the contraction in global $-Liquidity would slowdown, resulting in easier financial conditions which would support riskier assets like the rand.

“Keeping it simple”: There are many economic/financial variables that influence movement in the rand at various stages in the economic cycle, but the single most important macroeconomic variable that influences movement in the rand and other risky assets is the USD, according to our studies, as it remains the reserve currency of the world and lubricates global financial markets (carry trade).

If the USD (DXY Index) breaks below 95 or the EURUSD breaks above 1.14 on a sustained basis, it would signal that financial conditions are becoming easier than the market expects, and in this scenario (amid a lack of local exogenous shocks), the rand is likely to strengthen close to R14.00, with the risk of further strength towards R13.80. If the USD (DXY Index) breaks above 98 or the EURUSD breaks below 1.11 on a sustained basis, it would signal that financial conditions are tightening more than the market expects, and in this scenario, the rand is likely to weaken close to R14.50, with the risk of further weakness towards R15.00 and above.

As we write, the EM/ZAR carry trade is losing momentum, and a liquidity injection is needed to either ease financial conditions materially or boost investor risk appetite (Chart 2); hence, the next couple of weeks will be crucial.

At this point, we are closely monitoring the R14.50 level. If the USDZAR remains above this level over the next two weeks, there is a chance it could extend to 14.90, with the possibility of extending to 15.00 and above. If the R14.50 level holds, we will consolidate below this level over the next two weeks, and the rand could retrace to close to R14.20 For a technical perspective, please refer to “Technical FX Strategy: The EM currency bull trend since 3Q18 is over”.