Accessibilty Links

Executive Summary

The “double whammy” of a stronger Dollar and now the weaker Chinese Yuan is casting a shadow over financial markets; this has led to losses in the rand and other emerging market currencies. Evidence of this can be seen in the increased sensitivity between the moves in the USD/CNY and EM FX i.e. the beta (sensitivity) has climbed from 0.15 to 0.40.

The currency of the world’s 2nd largest economy – the Chinese Yuan – has slumped in recent weeks (YTD -4% vs. the USD), raising concerns that its over indebted economy (debt to GDP ratio currently at 257%) is slowing down which will pose a headwind for global growth, commodity prices and the outlook for emerging markets. A slowdown in Chinese growth is likely to tighten global financial conditions, and this will note bode well for the rand and other EM FX – Chart 1 and Chart 2 on the next page.

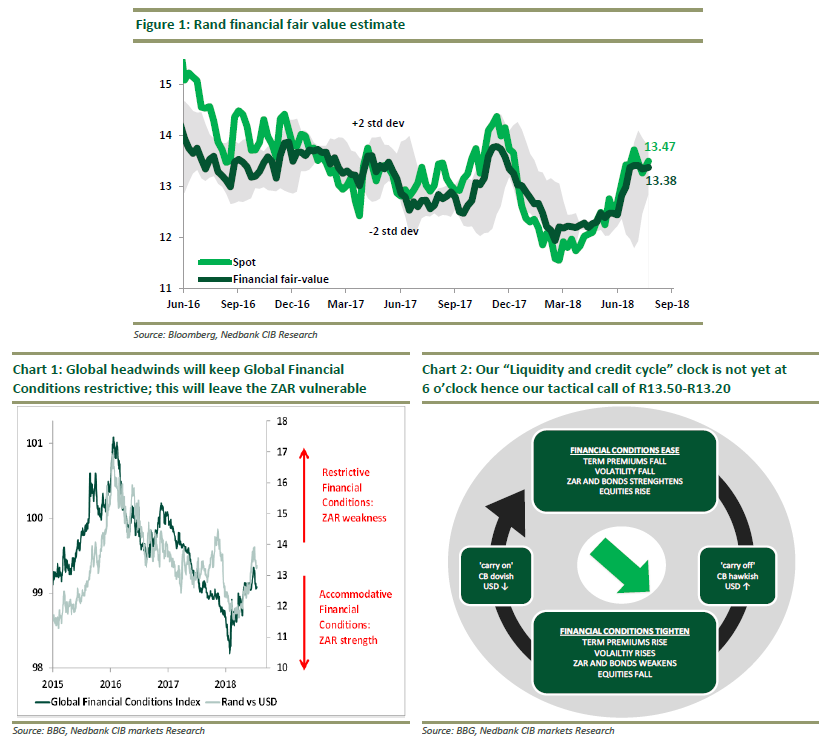

In light of volatile external developments we believe the rand is likely to remain in the range between 13.50-13.20 for the following reasons 1) hawkish language from the SARB 2) our expectations that Chinese authorities will intervene to ease financial conditions in its economy and 3) the US Dollar is struggling to break out of a tight range between 94-95 index points on a sustainable basis.

As mentioned, the SARB last week delivered a hawkish MPC statement despite keeping the repo rate unchanged. The MPC statement was more hawkish than we expected, not only in its language, but also via its forecasts. Our headline inflation forecast remains well below that of the SARB’s and as a result we do not expect the SARB to hike rates this year. However, the hawkish statement should provide some support for the currency in the near term in a volatile external environment (see Upping the ante in language and forecasts of 19 July).

Longer-term , we maintain our view which we have had since the start of the 2018:

Tighter global financial conditions will continue to dominate the outlook for the rand. We believe the longer term trend for the rand is weaker amid lingering trade-war risks, China credit cycle slowing down and as growth in $-Liquidity remains restrictive. As a result, we believe that the rand will end the year in the range of 13.00-14.00, with a bias towards the upper end of this range.

From a technical perspective, we recommend keeping an eye on the $-Rand resistance level of R13.17 and $-Rand support level of R13.37 (see our latest Technical Strategy note: “The first part of the correction is complete” dated 18 July 2018 for a more detailed technical view on the currency).